***Click here for an UPDATE – 2 years later***

I usually write in this blog about babies and breastfeeding and potty training and other cute and gross and funny and sentimental things. So I apologize in advance for this one. It’s about insurance.

STOP!

Don’t leave. I know insurance is not what anyone wants to talk or read about but please please please, I will sprinkle cute baby pictures throughout if you just hear me out on this one. It’s important. To me and to women everywhere.

See, our healthcare system in the US is pretty much fucked. And as much as I’d like to go all Erin Brockovich on this one and change the system it just ain’t. gonna. happen.

BUT there is one thing I might be able to change. And it starts with getting the word out since I’m willing to bet most people who have an infant at home just pay their medical bills and get on with it and don’t actually check to see if their insurance company is paying their fair share (spoiler alert: they’re not).

I know the last thing new moms have time for it fighting their insurance companies. I really, really know.

But do it anyway.

Do it anyway so the next generation of moms doesn’t have to.

So here’s the deal.

This whole battle started out over $590. Yet another bill for Lucy’s birth on top of the thousands I had already paid that I didn’t expect and couldn’t afford. My insurance company should have paid it, and yet again they were deferring the cost to me. My dad implored me to fight it, and I told him “I have a 2 year old and a 2 month old. some days I don’t have time to brush my teeth, how do you expect me to find time to fight a billion dollar insurance company?” But I didn’t have the money to pay, so I fought it anyway. I fought and fought and fought and finally, I won. I won the battle (they paid my bill) but not the war (they still aren’t paying other women’s bills).

In the beginning I said, I can’t be the first person to figure this out. I can’t be the first person who’s pissed. There are hundreds of new mothers across the country who are lawyers, lawmakers, legislators. Surely one of them has already tried and failed to defeat this. But that’s a dangerous way of thinking. Because if that’s what we all say, well, that’s how we end up here.

So I’m not a lawyer, I’m not a legislator, I’m not anything special but I am a mother and let me tell you, motherhood makes you fierce.

Ok, so here’s what’s going on.

Back in the day insurance companies billed for each OB appointment separately. Each prenatal appointment was a separate bill, then the delivery, the postpartum checkup, etc.

Then the affordable care act was signed into law and insurance companies were suddenly subject to a whole new set of mandates including one that required them to pay for all preventative care (i.e. prenatal visits) in full, without any member cost sharing. (In case you don’t speak insurance, that means they pay for the whole thing and the patient shouldn’t receive any bill whatsoever.)

But anyone that has been to the doctor since the affordable care act was passed knows that this pretty much never happens. They always find some way to charge you something – whether it’s covering the vaccine but not the actual giving of the shot (yup, that happened to me), or having a service covered but not available anywhere in your state (again, been there). All of their little workarounds piss me off, but this one really put me over the edge.

Now, they’ve come up with a way to avoid paying for prenatal preventative care.

Basically what they do is instead of billing each OB appointment separately, they bill the entire pregnancy in one “Global OB Fee” after the delivery of the baby. So they lump the prenatal visits, delivery and postpartum checkup into one bill – with one code.

And therein lies the rub.

Since all the appointments are lumped together into one bill, they code the entire thing as diagnostic care and apply it to the member’s deductible or cost sharing. Even though a large portion (arguably the majority) of the cost of that Global OB Fee is for prenatal visits, which are preventative and should be paid in full by the insurance company.

But instead of paying them, they combine it with the diagnostic service (delivery) and pass the cost on to the patient.

Hellz to the NO.

Because I’m cheap smart broke I go ever every bill with a fine tooth comb before paying it – and when I got a bill from my doctor after Lucy was born, I noticed something was off. NOTE: The bill you receive isn’t called a “Global OB Fee,” and you probably won’t see that phrase anywhere on it. That’s just how providers refer to this type of global procedure coding. The bill will simply look like a bill from your OB or midwife. Since the bill comes after the baby is delivered, most people mistakenly think it’s a bill for their doctor’s delivery fee, but in reality, all of the prenatal charges are lumped in there too. The only way to find out exactly what was included in the bill is to ask your doctor, or ask your insurance company how it was coded (there are 5 different global OB codes). In general, if the amount billed to insurance (remember, the amount that you actually owe is likely less) is over 1000 dollars, then it is probably a global OB fee, and not just a delivery charge. Also note that this fee is separate from the charges you will likely receive from the hospital and/or anesthesiologist. The global OB charge is specific to services performed by your doctor.

In my case, the total amount billed to insurance by my doctor was $2,950 dollars. That included prenatal visits, vaginal delivery and a postpartum checkup (I know because my doctor informed me of this upfront). My insurance company processed the bill as diagnostic care, and since I had already met my deductible (because for some reason an uncomplicated vaginal delivery + 24 hour hospital stay costs 15k dollars) they applied the entire amount to my member cost sharing. They paid 80% and left me with a bill for the remaining 20%…$590 bucks.

Hold up though.

A large portion of the $2950 that my doctor billed the insurance company under the Global OB code was for my prenatal checkups, which, according the ACA (and my insurance company’s benefits handbook) are considered preventative care. So according to the law, the cost of those appointments should be paid in full by the insurance company. The remainder (i.e. the delivery/diagnostic portion of the bill) should then be applied to my member cost sharing. This would have brought the bill down to somewhere between $200-300 bucks.

But instead, they billed the entire Global OB fee to my member cost sharing. NOT LEGAL.

To make a long story (sort of) short:

To make a very, very long story short, I decided to fight them. I did incredible amounts of research on the exact language of the Affordable Care Act, the benefits included in my specific healthcare plan, and how other insurance companies process and pay claims billed with Global OB codes. What I discovered is what I already knew – that these Global OB codes have created a conundrum for payers (insurance companies) in that they combine both preventative and diagnostic care under one code – and the insurance company’s software doesn’t know how to divide up the bill and pay it accordingly (full coverage for preventative, cost sharing for diagnostic). Whether this is an unfortunate outcome of a new system (yeah right), or an intentional workaround to avoid paying for preventative care (more likely) – it is ILLEGAL.

Some healthcare companies have already made changes.

I discovered that at least one major health insurance company (United Healthcare) has already implemented a percentage system in which they assume 44% of the Global OB bill is preventative care and 56% is diagnostic – and pay out the claims accordingly (i.e. insurance pays 44% and the remaining 56% is applied to member cost sharing). The following quote is from the United Healthcare benefits handbook, further reinforcing my assertion that applying an entire Global OB bill to member cost sharing is not legal.

The other (legal) option is for them to separate the bill into individual appointments and pay out each claim individually (like they used to do back in the day) – but this takes significantly more time for both the insurance company and the doctor, and in my case, Harvard Pilgrim’s own Provider Handbook states in no uncertain terms that doctors may not bill appointments separately (as described above), and instead that they MUST bill using the Global OB codes, or they won’t be paid.

I fought my way through three member services representatives and one supervisor before finally getting word that Harvard Pilgrim had agreed to reprocess my claim – and ended up paying the entire thing (not just the preventative portion) – more than they legally had to.

Why would they do that?

They paid my entire bill (instead of just the preventative portion) for two reasons. The first is that their processing software has only two choices for how to pay out a bill with just one code – preventative (pay in full) or diagnostic (apply to cost sharing). Since their own software wouldn’t let them divide up the global bill they either had to pay all of it, or apply the entire thing to cost sharing.

They opted to pay the entire thing because they realized it was cheaper for them to pay my bill then battle it out in court, and because if I took them to court and they lost, they would have to change the way they bill for everyone. A very expensive proposition.

The battle is won but the war continues.

So my battle with Harvard Pilgrim is over, but the war is not. They paid my claim, but they still aren’t correctly processing Global OB bills for many other women. And in order to get them to make a systemic change in the way they pay for obstetrical care we need to CONTINUE to put the pressure on them. And there are a couple ways we can do that:

- If you had a baby recently (or are having one soon), fight your insurance company AND FIGHT HARD to force them to pay their fair share of your Global OB bill. Even if it only saves you a few hundred bucks – it saves women collectively millions. Millions that belong in our pockets for diapers and daycare – not private jets for insurance company executives. (Here are Some Tips for How to Fight Your Global OB Insurance Bill)

- Contact your state legislator and ask them to hold insurance companies responsible for covering preventative obstetrical care as required by law. I’m meeting with one of my state legislators next week to discuss this very issue.

- Share this post to bring attention to insurance companies that are circumventing health care laws and get it in the hands of influencers like the media, legislators, lawyers, etc.

Get in touch.

If you have questions about an obstetrical bill from your insurance company, you’d like help fighting your Global OB Fee claim, or you know someone who you think could help bring attention to or enact legislation to create change, feel free to contact me directly!

I know this probably seems like an itty bitty bandaid on an incredibly broken healthcare system. But I can’t change our healthcare system overnight. I might be able to change this.

Good job! This stuff is so complicated and bull shit. Global payments make a lot of sense, but we aren’t doing it right in this country. The ACA was a step in the right direction, but our politicians really need to have the balls to move to a more simplified (ahem socialized) approach. Cover everyone for all preventative and emergency care (deliveries included) and then we can buy insurance for the extras.

I so agree, Amy!

YOU GO GIRL! Kudos to you for taking the time to inform your peers of this issue and not assuming that a little battle won does not contribute to fighting the war! Aunt Annie

Good for you for standing up for your rights! I just got a letter saying that the global code procedure was accepted, yet I got a bill for previous services. Already, I am dealing with contradictions. My insurance at first told me I had a co pay when I see the co pay each time, but further details say if it’s preventive it’s zero co pay..they put me on hold, and come back and say yes, every visit is zero copay. I asked about ultrasounds..they said co pay wasa like 30 or something, i asked what if it’s in office and the ob wants to do it during the prenatal visit, and since u are seeing the ob for preventive, wouldn’t that be preventive since he ordered it? and they said yes, so zero copay in that case. Now, I get a bill of 30 and I will continue getting it every time I go to them. The billing lady said my insruance told her it’s 30 a visit and I said that’s because it’s generic and if they dig deeper, they will find out its not bc of preventive etc..she said well what u got done isn’t preventive. I’m like what?? I said according to ACA, prenatal visits are well woman visits and well woman visits are preventive. Shes like we don’t consider them well woman visits, just regular visits. And she said besides that, when you do your first visit, it’s not prenatal it’s first time established patient, and besides that, ultrasounds are not preventive and you would get charged anyways for that. I told her what my insurance said and she said, well if they send us a fax saying it’s zero co pay for all the ob visitis, then we will put that in the file so u don’t keep getting charged. I spoke to claims and she claled up my plan and said they told her same thing, preventive prenatal care visits are zero copay, but to what is censidered preventive is basic in what they told her. ie they didn’t even tell her urine tests and bloodwork etc. So, she is going to call the billing to see what they are saying etc.. I told her that it sounds like the woman is not coding it as well woman nor preventive and not wanting to code it correctly. She didn’t seem concerned about what i said about aca etc. I’m thinking, well, I didn’t ask for hte ultrasound, the dr ordered it so I would think that’s preventive as he saw it necessary to do it?? My first visit at ten weeks they ordered a transvag and ultrasound and the 2nd one at 12 weeks an ultrasound..but i saw a procedure code for the nuchal something and he ordered bloodwork each visit i went and did all the blood pressure urine test fetal heart uterus measuring etc. What’s odd is hte bill they sent me doesn’t show global coding nor the nuchal one for the ultra sound..it just shows the codes 99203 (new pt interm ov), 76856 (pelvic ultrasound) a, 76830 (utz transvaginal), 99214 estab pt interm ov and 76801 (ultrasound ob 1st tr)…but yet i got an authorization approval from my insurance for codes 76813 (ob us nuchal measure 1 gest) same day as my 2nd visit, andm 59400 (two times two different days of referral and two different referral numbers for same two codes) for routinge ob care inc atempartum care , vag delivery and post partum care. does that mean as well that if i need a c section it wont be covered?? i know in my plan it says zero co pay for c section. and 600 co pay per hospital admission. so i am curious if you have ot pay for your ultrasounds including ones for nuchal and first visit? and what u recommend i do?

Hi Melissa, thanks for reading and I’m sorry you are going through all this! Insurance is so complicated While I am definitely not an expert and all insurance plans are different – I’ll tell you what I know from my own experience and time spent sifting through various ACA regulations.

While I am definitely not an expert and all insurance plans are different – I’ll tell you what I know from my own experience and time spent sifting through various ACA regulations.

It sounds like you are currently pregnant and haven’t delivered yet. In that case you likely have not received a global OB bill yet. That will come AFTER your delivery. Included in that code/bill is typically all of your prenatal appointments (note that it is just the appointment fee – any tests or ultrasounds you receive at those appointments will be billed separately) as well as your delivery fee. You will be billed separately for your hospital stay (if applicable) as well as anesthesia or any other drugs you receive in the hospital. The Global OB fee is just for the prenatal appointments and delivery services provided by your OB. The thing to look out for when you receive that bill is to make sure that at least 40% of the global OB fee is paid for by insurance BEFORE they apply it to cost sharing. At least 40% of the global OB fee should be considered preventative, and therefore not subject to cost sharing. For example if your global OB bill total was $2000, at least $800 (40%) of it should be paid by insurance, and only $1200 (60%) should be subject to copay, deductible or coinsurance.

You asked about the global OB code including vaginal delivery but not c-section – that is just because the doctor has to choose one global OB code to use (there are different codes for vaginal delivery, c-section, twins, etc) and he or she is anticipating that you will have a vaginal delivery. If you need a c-section they will simply change the global OB code to one that specifies a c-section. Both vaginal and c-section deliveries are considered diagnostic (not preventative) care so you will be subject to cost sharing for those services. However, if your insurance plan specifies no copay for c-section than you should not be charged for it. The $600 copay for hospital admission will be billed separately by the hospital.

As far as the ultrasounds – ultrasounds are not considered part of a well-woman prenatal visit. So the actual visit with your doctor (checking blood pressure, measuring your belly, listening to the fetal heart rate, etc.) is considered preventative and would not have a copay – but diagnostic services you receive during those appointments (for example urine tests, blood tests, ultrasounds, etc.) are all considered diagnostic and WOULD BE subject to your copay. That is probably why you are seeing those charges. That said, all doctors code those services differently. My first baby my OB coded the ultrasounds as preventative and so I wasn’t charged. My second baby I had a different doctor and he billed them as diagnostic so I did get charged. You can ask your doctor to change how they code it – but according to the law they don’t HAVE to bill ultrasounds as preventative. The ACA only specifies that the actual appointment is preventative. There are certain services like STD testing, gestational diabetes testing and routine urine protein testing that ARE included in the ACA as preventative care for pregnant women, so you should not be charged a copay for those services, and if you are I would absolutely appeal the charges with your insurance company. However things like blood tests and ultrasounds (even though they are routinely ordered by your doctor) are not considered preventative under the ACA. You can see what tests are specifically covered as preventative here: https://www.healthcare.gov/preventive-care-women/. If you have been billed for any of the services listed there, I would show that list to your insurance company and ask them to reprocess the charges.

Again I know this is super complicated and SO frustrating. You are smart to be looking closely at all the charges and keeping track – I know it is time consuming!!! If you have any other specific questions I am happy to help you research them and appeal the charges with your insurance company if necessary. Good luck and congratulations on the new baby – let me know if you have any questions once you get the post-delivery bills 🙂

diseases, genetic,etc or maybe because I’m 35, so the dr said like the genetic testing ones etc. are covered because of my age. The reason I am being charged 30 is because of the billing lady is coding it as new patient visit and established patient visit instead of i dont know what they would code it as, but for the well woman prenatal preventive. I even typed in teh codes online and thats what they came up as normal visits. My friend works at an ob office and said I shouldn’t be charged for every single visit. but the billing lady said she would charge me for every single visit of 30 until she gets something from my insurance saying what i told her they told me. She told me they told her my maternity plan is 30 for prental visits and i said, yes, but it also says for NON preventive services..and shes ike, well these are not preventive visits and not well woman we charge are normal etc. There’s a helpful website I came across the breaks down what is included in a well woman prenatal visit or examples. http://www.healthlaw.org/issues/reproductive-health/well-women-visits-prenatal-care-under-the-acas-womens-health-amendment#.WKdzHfkrLIW.

So with global coding, u are saying I should only have to pay one co pay and not for every single visit? My insurance works with copays not co insurance. and i wnoder how that works since the dr visiting me at the hopsital is zero copay, surgeons, anestheologists etc are zero copay, but hospital including maternity is 600 co pay. Update: I tried to speak to 2 different women with insurance and one lady finally saw what i saw saying she “said” and was going to call up the billing lady with me, but they were closed..and yet she noted that i “think” i should have to pay zero co pay when i told her they can listen to the phone call and told me that is what it should be lol. and she referred to the 30 co pay lol. My hubby was like, what??? that’s unprofessional. the other lady i spent over an hour with arguing with her, and pointed out that it even says preventive services for pregnancy are zero co pay, and she told me those are for birth control etc and i’m like, no that’s a different section all together and thats not what the other reps said. Let alone it says well woman is preventive and shes like thats your yearly and i told her according to law, prenatal visits are well woman. shes like well your policy doesn’t go by that lol, but yet, if you look it says they go by aca and hrsa lol. so i asked to speak to a supervisor but i dont know if she was lying or not but she said he was at lunch adn would call me when hes back or today. and she said she understands my frustation and shes just hte middle man but almost said it like i was wrong though i told her thats what the reps told me 2 x. but yet the insurance companny puts basic notes down is client asked about prenatal care 30 copay and left out the part they said zero co pay for preventive services lol. i’m like u can listen to the phone call and hear them! and i told her yes its frustrating etc and she hung up.

Hi

My name isSarah and I received a global billing change that I have been fighting! I would love to talk with you and pick your brain. I just hired an attorney and would love to just ask you questions! How can I contact you?

Thanks so much

Hi Sarah,

I would love to chat with you. Go ahead and send me your email (or you can send it via direct message on Instagram – @ohbabyrichards) and I will be in touch!

Hannah

Hey Hannah,

I currently live in VA, and my OBGYN office is actually trying to get me to pay my Global Fee (letter states OB Payment agreement) now (February) and I am not due until August! They admit it is all the prenatal office visit with the provider delivery fee. I’ve been denying to sign the agreement because I do not believe in paying for something that has not happen yet. Not to mention, I have a health savings account that I can be using, by since they dated it 12/2021 and not of 2022, I cannot even use it towards this Global even if I wanted to. They said they could reimburse me, I explain to them I was not doing all that. I keep getting the run around. I am doing my best to stick to it. But now, thanks to your post. I have more research to fight to get them to bill each appointment. As for my insurance, prenatal care visits are like preventative care visits.

It is just frustrating to have to deal with this on top of growing a baby and preparing for the baby’s arrival.

Hi Brooke, sorry you are dealing with this. Unfortunately it is pretty common for OBs to pre-bill their global OB fee. They do this to protect themselves, because the insurance companies won’t let them bill (or get paid) for any services until they submit the global OB bill AFTER the delivery. So providers are essentially going 9-10 months without getting paid. While you might be pre-paying for the service now, the actual claim will be dated with your delivery date, so it shouldn’t be an issue from an HSA perspective. While I know it’s pain to have to pay in advance, your doctor is within his or her rights to do this, so if you truly don’t want to pay up front you may have to find a new OB that doesn’t pre-bill (although I think that would be tough as most of them do this). The key here is to make sure that once you give birth, your insurer is paying their fair share of the bill. Once the insurance company pays, your doctor will reimburse you for anything you paid them over and above what is due from you (i.e. your deductible/cost sharing).

My advice would be to keep all receipts for payments made, and request an itemized statement of what is being billed and/or included in the global fee. When your insurance pays the doctor after delivery, request to see the EOB (explanation of benefits). If the insurance company isn’t paying at least 40% of the global OB fee (which is for the preventative prenatal care portion) than you have a case against them.

Unfortunately, your doctor is kind of trapped in the middle – he or she isn’t doing anything wrong by charging a global OB fee, and they are smart to try to collect it up front since insurance companies so often don’t pay it – even when they should be. So if you love this doctor I would pay the upfront fee and make sure to fight your insurance company afterward if they don’t reimburse you.

You could also attempt to talk it through with your insurance company up front and confirm with them that they are going to be paying at least 40% (the preventative prenatal care portion) of your global OB fee (if they say they aren’t paying the preventative portion I recommend reading through some of the responses I’ve made to other comments for advice on how to fight them). If you can get in writing from the insurance company what portion of the global OB fee they will cover, you can take that to your doctor and they may lower the amount you have to pay up front since they have confirmation from the insurance company that the remainder will be reimbursed.

Good luck, and let me know how you make out!

ahh sorry it cut off the first half of it lol. Thanks for all of your help 🙂 That’s the thing is the insurance flat out told me ultra sounds were covered for pregnancy stuff ie not like normal ones and the first one he did because at 10 weeks taht’s the only way he can measure the uterus and hear the fetal heart beat and getstational age etc. and the 2nd one, was for nuchal US, which goes with the genetic testing , but i did read somewhere i wanna say that bloodwork is preventive such as blood group RH and diseases etc, but maybe because of my age is why.

I’m so sorry, Melissa that is so frustrating. If your insurance states that you should have zero copay for a service, then definitely do not pay the bill until you have worked it out with your insurance company. Once you pay it is hard to get your money back so I would withhold payment until a resolution is determined – that will incentivize your doctor’s office to work it out with insurance so that they can collect their money.

It sounds like you are doing all the right things to fight this. You definitely should not have to pay a copay for regular prenatal checkups. Those checkups are included in the global OB fee and under the ACA are required to be completely free (no copay). Other services provided at the appointment might have a copay, but not the visit itself.

As far as the ultrasounds go they are not required to be covered as preventative (no copay) by the ACA, BUT if your specific insurance plan says that they are covered with zero copay then you should not have to pay one. As you move forward fighting your insurance company/doctor’s office on this issue I would ask for everything from your insurance company in writing so that you have written documentation of what they are telling you, and then submit that to your doctor’s office. You can also request a 3-way phone call between you, your doctor’s billing representative, and an insurance representative – that might help with the miscommunication.

Lastly, the insurance company’s most effective tactic with stuff like this is making it drag on for so long that people just give up and pay the bill. They never call back when they say they will, and it feels like each representative you talk to is starting from square one. I recommend asking for each representative you talk to to give you their name and direct phone number so you can talk to the same person each time. When they know they can be identified they also tend to be a little more helpful. At some point if they continue to stall and not help you, you can tell them you will be submitting a claim to the state insurance board – that usually kicks them into high gear since they don’t want to deal with the insurance board.

Good luck and let me know how it goes!

This was so on time. I’d like to speak to you more on this if possible. Please email me jasmine.stephens@gmail.com

Hi Jasmine, thanks for reaching out! I sent you an email at the address you provided. Hope it reaches you 🙂

Hi Hannah, I had a similar experience with my ob except it hasn’t come to the delivery part yet. I’m half way thru my pregnancy now and have already done some bloodwork during my routine prenatal visits at my OB’s office. Some of the tests they did were HIV testing, Hepatitis B, Rh incompatibility, rubella, STD, etc. I saw they are listed by the ACA as preventive testings for pregnant women and should be covered by insurance company without member cost-sharing. HOWEVER, I got a bill from the lab where the OB sent my blood to that says I owe them the entire thing. The EOB I had also indicate insurance paid nothing for these tests. Everything is on me. I was shocked and called around both the insurance and the doctor’s office/lab to figure out what’s going on. Basically the ob billed the insurance these tests under a different name called “obstetric panel” and did not listed these tests separately. Thus the insurance won’t recognize these tests and then considered them as non-preventive and therefore has to go thru my deductible first. I then asked the OB’s office why they didn’t bill them as preventive tests. Guess what they told me? They said they billed them as “pregnancy” not preventive because that’s those tests were for – for my pregnancy visit….They refuse to either bill them separately or bill them as preventive care because they think these tests are for pregnancy AND preventive care and pregnancy are two different things! I don’t know if their argument is legit from a coding perspective but it doesn’t make any sense to me. What should I say to them cause now the OB’s office is blaming my insurance for “don’t like the way the tests are called”; and the insurance insisted on that the tests my Ob billed do not fall under those listed by the ACA because of the names.

Ugh , Audrey – so frustrating! I had the same thing happen to me. Unfortunately there is no easy solution except to keep fighting them tooth and nail. The insurance company is betting on the fact that you will eventually cave and just pay the bill, which is what most people do. What I did in this situation is ask my insurance company representative to initiate a 3-way call with insurance, myself and my doctor’s billing department. On the call I made sure everyone understood that these specific tests were required to be covered per the ACA and asked my doctor and the insurance company to discuss (with me on the phone) exactly who needed to do what to make that happen. Basically if you try to be the go between with the doctor and insurance they will keep telling you the other one is doing something wrong – if you get them on the phone together it requires them to hash it out. Ideally you ask the insurance rep to tell the doctor exactly what code the tests need to be billed as in order to be covered as preventative. I told them “I don’t care what you do or who does what but you better figure out a way to make this covered or I am filing a complaint with the insurance commission!”

Another tip is to be insistent that the insurance rep you’re speaking to transfers your call to a manager. Often the first line representatives don’t really understand the law and the coding issues. Keep insisting that you speak to a manager and if they tell you one will call you back, call every single day and tell them you are recording each call. I actually looked up the customer service manager for Harvard Pilgrim in my region on LinkedIn and called her directly! That was when things finally started to get handled.

As a last resort, you should absolutely file a claim with the insurance commission in your state. Once the insurance commission comes nosing around your insurance company will likely just pay the claim to get them off their backs.

Good luck and let me know if I can help with anything else!!

I love this and am about to have my baby any week now. I don’t know what my member sharing is and I have a $0 deductible , a $5k out of pocket max than everything is 100% covered. My copay for hospital stay PER DAY ( I pay $500 a month and an almost their top plan 🙄) is $600 at max if $1800. That’s INSANE. ( I have florida blue ).

So, my which I knew bullshit “global fee” is $4,300 for my doctor. But I paid like 4-6 $60 copays for my visits between 18-26 weeks then I suddenly did t have anymore? Do I ask my dr office what’s up with that ? I thought bc of this global fee crap, i shouldn’t have to pay.

I just looked at my current claims and I paid $183 for my nuchal translucency ultrasound in first trimester which I thought was under prenatal care for the ACA ?

Hi Jen, unfortunately ultrasounds are not required to be covered as preventative under the ACA so it all depends how your doctor bills the appointment. Looks like they billed it as diagnostic. Let me know if you have other questions, though!

Hi Jen,

It’s hard to know without having all the details of your plan and what exactly the copays are for and whether or not you should have to pay them. Each insurance plan is different, but I do know that regular prenatal checkups should be covered 100% by your insurance without any copay or deductible (and they are typically included in the global OB fee). However, there are sometimes other costs like blood tests, ultrasounds, etc. that are not considered preventative and can incur additional costs during your pregnancy. I would ask you doctor and/or insurance company for a full explanation of what the copays are for so that you can understand whether or not you need to pay them. Good luck with your pregnancy!

That make sense I paid for ultrasounds ; which is another convo about now they’re not included in “prenatal care” and those appointments went towards my out of pocket expense anyway.

Why I’m concerned about and have been- is how they’re billing things as this global fee when it shouldn’t be lumped together. Those services all need to be separate so that the insurance company will pay the proper amount correct? Since many of those fees aren’t associated with actually giving birth but of care of me the patient prior to it?

Before This “global bill” is laid- do I request my doctors office to break down every code since that is HOW insurance works? Every thing they do – needs to have a CPT or diagnostic coding attached to it. There is not ONE code for all of that. Which I was already well aware of. Do I also ask my insurance what my cost sharing is?

Hi Jen, you’re right about the global code and all the codes getting lumped together. That’s the big issue I had. Unfortunately asking your doctor to break up the codes usually doesn’t work because most insurance companies actually require the doctors to bill using a global OB code. So what I would do is for sure find out from your insurance company what your cost sharing is, if you have any. All plans are different, some have deductible and then cost sharing, others go directly to cost sharing. The key is going to be when you receive the bill for the global OB fee, making sure your insurance company pays at least 40-50% of it. The global OB fee includes both the delivery and the prenatal visits. The delivery portion IS subject to cost sharing but the insurance must pay for the prenatal portion in full since that is preventative care. So when you get the bill make sure they paid at least about half of it outright before applying it to cost sharing. If they didn’t that’s when you need to call and contest it.

Also- is there anyway you can upload your global bill etc to your post ( blanking out any personal information) so that we are able to see the information you are talking about? That way, we can apply what you’ve said and see what you’re referring to? And thank you so so so much for writing this and answering our questions.

Hi Jen, I’ll have to look through my records to see if I can find the bill and share a picture of it. Keep in mind that it will look different for everyone, though, depending on how your insurance plan is structured. I had a $3500 deductible and then 80/20 cost sharing for my plan. I’ll see what I can find though for reference. Also just curious… I’ve been getting a lot of traffic to this blog post recently (which I wrote about a year ago) so I’ve been wondering where it was posted that so many people are now seeing it. I’m really glad it’s helping people, I just can’t figure out where the traffic is coming from! Do you mind sharing how you found the post?

Thank you again!

I will absolutely make sure that happens when I get the bill that it is paid correctly. I don’t have a deductible, so I’m guessing it will go to cost sharing ? Is that also known by your schedule of benefits ( coinsurance)? If so, mine says 60/40? Other than that I’m not sure what it would be, and every time I’ve tried to talk to my Insurance I get transferred and they can’t answer any of my questions.

Anyway ! Haha I think I googled “does global ob fee include copays ? “. It came up on AMP/ word press on google search ne’er the top.

Hi Jen, if you have no deductible then your coinsurance is the same as your cost sharing. So, when you get the bill what will likely happen is insurance will pay 40% and tell you to pay the remaining 60% – HOWEVER – what they SHOULD do is pay at least 40-50% of the bill outright (the preventative care portion), and then pay 40% of the remainder (diagnostic). They probably won’t do this on their own, which is why you will need to call and argue with them about it. The front line reps probably won’t know what you’re talking about so you just have to be super persistent and keep asking to be transferred to a supervisor. Make sure you threaten to file a claim with the state insurance commission, that seems to help. I have some more tips on how to win your case in this post (https://ohbabyrichards.wordpress.com/2016/07/19/how-to-fight-your-global-ob-fee-bill/) but feel free to reach back out for help!

It says that my part should be 40% for covered services. I will absolutely keep at them if they are not doing whag they are legally required to do. Again, thank you!

Hi Hannah,

I was so happy to come across this! I am having a baby due January 2018 and I was handed a global bill by my doctor and asked to start making payments to be paid in full before my delivery. When I questioned why prenatal care was being lumped into this bill with delivery and postpartum care I was told that is just how they bill it and that prenatal care is never really paid in full by the insurance company anyway. So, I started my research and came across your blog. I contacted the person that is supposed to help with insurance through my husbands work and my insurance company directly. I told both parties that I know prenatal care should be covered by insurance without any cost sharing on my end per the “womens health amendment”. Both parties acted confused and as if they had no idea if prenatal care is actually considered “preventative care” and they also told me that my doctor has to code the appointments the correct way in order for them to pay the claim correctly. Help! What should I do? Where can I get confirmation that prenatal care is supposed to be covered in full without cost sharing? I looked at the HHS.gov sight and all it says is “well woman” visits. There is no actual mention of prenatal care than I can find. I also looked at my explanation of benefits and it says I owe a $25 co-pay for each prenatal appointment which is also incorrect according to the ACA, correct? All I want to know from my insurance company is that prenatal care should be covered in full without cost sharing and how to communicate that to my doctor so I’m not paying more out of pocket up front than I have to. This is so maddening!

Hi Amy,

I’m so sorry to hear that you are still fighting this same annoying fight and that insurance companies are still trying to evade their responsibilities around women’s healthcare – ugh! Your doctor is correct that they are required to bill using the global OB code – it is up to your insurance company to divide it up and pay the preventative portion in full, and then apply the non-preventative portion of it to your plan’s cost sharing. This is where you will likely have to fight them. In terms of convincing your insurance company that prenatal checks up must be covered without cost sharing (you should NOT be charged any copay whatsoever for the prenatal visits unless the copay is for diagnostic testing that was administered during the visit) you can use these links. The first link (https://www.hrsa.gov/womensguidelines/) outlines what services MUST be covered as preventative care. You will see that many of the tests you receive during pregnancy such as immunizations and prenatal diabetes screenings should all be covered in full without cost sharing. That list also includes well-women visits. You can see that there is an asterisk in that column that says that the frequency of well woman visits is dependent on a women’s health status. A healthy (non-pregnant woman) only gets one visit per year, but pregnant women are entitled to additional covered well-women visits (i.e. prenatal checkups). If you look at this second link (http://www.healthlaw.org/about/staff/susan-berke-fogel/all-publications/well-women-visits-prenatal-care-under-the-acas-womens-health-amendment#.WZ2k2XeGMmI) it breaks down the subtext of the ACA bill which specifically states that women require multiple well-women visits during pregnancy, and that even more well-women visits are warranted for high risk pregnancies. Take a look at the text in here and present it to your insurance company as evidence of their responsibility to cover the prenatal visits (and other covered services during those visits) in full. Let me know if you have further questions – but definitely fight them on this one, the law is on your side!

Thank you so much for the information, Hannah!! I really appreciate your help getting this figured out.

Unfortunately, I am having the exact issue as Amy. I found what you are talking about on the health law site (http://www.healthlaw.org/about/staff/susan-berke-fogel/all-publications/well-women-visits-prenatal-care-under-the-acas-womens-health-amendment#.WZ2k2XeGMmI) where it breaks down how the ACA should be interpreted, however this link that is sourced on that page ‘https://www.hrsa.gov/womensguidelines.’ is broken.

I think this is the new link https://www.hrsa.gov/womens-guidelines-2016/index.html

Do you know where I can find the actual OIM report?

From the healthlaw.org webpage “To implement the Women’s Health Amendment, HRSA commissioned the independent Institute of Medicine of the National Academies (“IOM”) to conduct a scientific review and provide recommendations on specific preventive measures that meet women’s unique health needs and help keep women healthy. The IOM identified eight women’s health preventive services. HRSA adopted all eight of those IOM recommendations and issued “Women’s Preventive Services: Required Health Plan Coverage Guidelines” (“the Guidelines”).[3] As a consequence, well-woman visit(s) are a type of preventive service that health plans must cover without cost-sharing.[4]”

So its stating the Guidelines came from the OIM report, but the actual guidelines referenced above are not clear or specific enough that I think I will make much headway using them alone.

“The Women’s Preventive Services Initiative recommends that women receive at least one preventive care visit per year beginning in adolescence and continuing across the lifespan to ensure that the recommended preventive services, including preconception, and many services necessary for prenatal and interconception care are obtained. The primary purpose of these visits should be the delivery and coordination of recommended preventive services as determined by age and risk factors.”

Hi Audrey,

This is a tough one because it has been left a little vague, giving insurance companies room to misinterpret it. However, at a minimum, any prenatal visits in which you received preventative services such as gestational diabetes testing, urine culture, etc should be covered because they are “delivering/coordinating recommended preventative services as Defined by age and risk factors.”

If your insurance company still doesn’t budge I would do two things: 1. Read through the language in your actual plan – my plan (Harvard pilgrim) actually spelled out in their own plan documents that prenatal visits were covered without cost sharing. They still didn’t cover them initially but when I presented them with their own plan documents they didn’t have much room to argue, although they tried. And then 2. Contact your local insurance commission. If your insurance company isn’t following the “good faith” of the law (ie using a loophole in text to avoid the intention) the insurance commission can encourage them to reconsider an/or advise you of your legal options to fight them. Since a large number of insurance plans do interpret pretanal care as preventative measure there is legal precedent for you to win a case against them.

I’m so sorry you’re having to go through all this. Good luck!

Hey Audrey, one more site I came across in my research today that might help: https://www.hrsa.gov/womens-guidelines/index.html

This site spells out that well-woman visits must be covered and that more than one may be needed annually for women to receive all of the recommended preventative services for their age and health status. You can also click the note to read some additional verbiage about how those additional visits should be determined. Here is what is says: “Section 2713 of the PHS Act and its implementing regulations allow plans and issuers to use reasonable medical management techniques to determine the frequency, method, treatment, or setting for a recommended preventive item or service, to the extent this information is not specified in a recommendation or guideline.” So basically, they are saying that doctors and plan providers can use reasonable medical judgement as to the schedule of preventative services.

I would think you may have some legal standing if you wanted to take them to court and say that any reasonable medical professional would recommend multiple prenatal visits for a healthy pregnancy – in fact the national guidelines for prenatal care specify exactly which schedule of visits and tests a pregnant woman should receive. However, I know that taking an insurance company to court is a big undertaking.

Another argument you may be able to use is that the language in the link I sent above pretty clearly specifics that appointments needed to receive the specifically identified preventative services for pregnant women (https://www.healthcare.gov/preventive-care-women/) must be covered as preventative care. So you may be able to argue that any prenatal visits related to those services must be paid at 100%. However, they will have to figure out how to separate those services from the rest of the global OB bill which will be a challenge for them. I suspect if you push hard enough you may get them to just pay the global OB bill because they won’t want to deal with you badgering them. You will have to fight them hard, though, the process for me was weeks long as detailed in my blog.

I would also contact your state insurance commission and raise the issue with them and see what they say. They have lawyers on staff that can help you work it out with your insurance company – AND – if you bring to their attention the issue of the vague language in the ACA requirements, they may even help to clarify the laws in your state.

Hopefully that is a little bit helpful? Healthcare in our country is such a mess!!

Thank you for your reply! I’ve actually only had 2 appointments and am not due till May of next year, so I’m wondering if now or then seems better to fight it? There’s a chance the representative and supervisor were incorrect and they pay for it no issue, because this is on their own website under the preventative care section.

https://www.blueshieldca.com/preventive-care/on-track.html

(Click female, 20-49, then it asks if you’re expecting and if you click yes it lists things you should be asking and doing at your prenatal appointments).

I was told yesterday by a supervisor that nothing (yes, NOTHING) in pregnancy is considered preventative, but I just wonder if she is uninformed. I also hate to fight and ‘win’ only to have to redo it all once I’m billed incorrectly with the Global billing! Or of course, there’s always a chance I’m billed correctly, which in that case I sure wasted a day yesterday looking at all that LOL

Hi Audrey,

I just found this today and thought it might be helpful to you when fighting your insurance company. The fact that they told you nothing in pregnancy is considered preventative care (and wrote that in their handbook) is in direct violation of the ACA. The link below quotes the exact text from the IOM report and states that all prenatal well-woman visits MUST be covered without cost sharing beginning December of 2016. If your plan year started before that date, it may be grandfathered until your new plan year starts, but if they change(d) the plan or price AT ALL in 2017 they will be required to adopt the new rules. You should be able to fight them with this! Good luck!

http://www.healthlaw.org/issues/reproductive-health/well-women-visits-prenatal-care-under-the-acas-womens-health-amendment#.WilmnhNSxTY

Thank you for such an informative post! I had no idea what global billing was & your blog explained it so easily! My dr.’s office does global billing as well and I have a few questions that they can’t seem to answer- of course they send me to my insurance, who sends me back to them…. I have an extremely high deductible at $4,500 (pretty much double what the dr.’s global billing estimate was!) and am due in March, 2018 (next year- aka another deductible due). Will my insurance hit me with the deductible twice when they get the global bill (since the services were provided in 2017 & 2018)? Or does it go by the date on the claim/when the bill is processed (when I give birth in 2018). Basically, I’m wondering if I could switch plans come Jan. 1st to a lower deductible plan (same insurance company & same provider) to help avoid having to pay $4,500 in general (much less x2!). Or would that not really work? Seems like the insurance company would have found a way to make that a no-go? Thank you!!

Hi Becky, it’s possible that each insurance company does it differently but I can tell you that my insurance company processed the global bill with a date of service of the delivery date so if you switch plans you should only have to pay the global bill once (applied to your new plan’s deductible). Also remember that your insurance company must cover at least 40% of the global fee in full (preventative care) and then the rest would apply to your deductible. They likely won’t pay the preventative portion unless you fight them on it but I hope you will! They are required to cover preventative care in full under the ACA.

thank you! I just spoke with the billing at my dr.’s office and she said the same thing and also encouraged me to switch plans at the end of the year as well! You are awesome!!

Thanks so much for your informative post! I was about to give up and pay the bill. Now I feel empowered to fight them!

My insurance does require a global code for all prenatal visits only. But my delivery date was right after the policy year restarted so most visits would have been covered because I already met my deductible the previous year if the visits were filed separately on the actual date of service but with the global billing after delivery, everything is applied towards my deductible and now I have a bill for prenatal visits over $1000. Now I see they should cover it 100%. Will call them tomorrow! Thanks!

Yes! Definitely fight them on it. Just know that if your delivery was also included in the global fee you WILL be responsible for that portion of the bill. Your insurance, however, should cover all routine prenatal visits in full per the ACA.

Hi Hannah

Just wanted to give you a quick update. Premera called back and said they are 100% compliant with ACA and they think I am confused in thinking prenatal visits are considered well women visits which should be 100,% covered. They said I can appeal and that’s it. I’m going to file a claim to the WA state insurance commission. Hope they will be on our side!

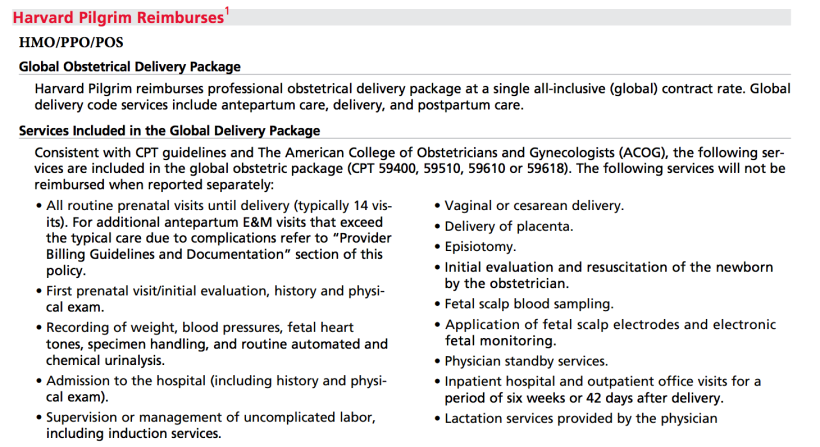

Good for you! Definitely file an appeal because they absolutely are required to be covered. Also make sure you review your specific insurance handbook to see what they say about prenatal visits. Even though Harvard Pilgrim initially told me they didn’t have to be covered as preventative, when I read them back their own handbook (which stated they were preventative) they changed their tune.

My bill was actually split into prenatal visits and delivery. Prenatal visits were counted as deductible. It just happened that our policy year restarted towards the end of my pregnancy and I had already met my deductible before all the prenatal visits. So if they had billed each individual visit separately, then they would have to cover 90% of these visits before the policy year restarted again, even according to their non ACA compliant policy. But of course requiring providers to bill globally ( even just with one global prenatal visits bill) they count on deductible to pay less.

Also I just found some text in united healthcare’s handbook that explains in plain text that the ACA does require insurers to cover prenatal checkups as preventative. You maybe be able to use this to help educate your insurance company. Send me your email and I can send it to you.

Thanks for offering to send the united health doc. I have the file and gave it to premera in our initial argument but they basically said another company’s internal file doesn’t mean anything to them. 😦

I have had this same issue and been fighting United HealthCare for the last few months on their global billing policy for prenatal care. I really appreciate this blog! Even though the info about the Affordable Care Act is posted on their web site, they still have refused to cover my claim for the initial lab tests and initial OB visit. They don’t seem to follow their own policies! I’m still working on it (while exhausted in the third trimester)!

Hi Elizabeth,

I’m sorry you’re having an issue with United Healthcare paying for prenatal care. They should absolutely be paying (in full) for your prenatal visits. Only a couple of lab tests are required to be paid for in full, though (per the ACA), so it’s possible that the lab tests you’re referring to could be subject to deductible or cost sharing. If you have questions about specific tests feel free to send me an email and I can try to help!

This blog is a godsend and I am so glad I found it. Like others said, I was just about to give up (and max out my credit cards). Thanks for taking the time to write this.

So glad you found it helpful Emily!

Hi Hanna,

I have update to report. I filed the complaint to the commissioners office. Premera reached out and basically said my insurance is a self-funded group policy and doesn’t have to comply with ACA. Have you heard such a thing?

Great job filing the complaint, hopefully the comission will be able to help you work with your insurance company to figure it out. As far as being self funded, it’s true that self-funded plans do not have to comply with all of the ACA mandates, however, they ARE required to comply with the preventative care mandate, which requires them to the cover preventative care 100% with no cost sharing to the member. The only exception to that would be if your plan is “grandfathered.” To be grandfathered, your plan would have to be exactly the same (i.e. no changes to the plan OR your premium) as it was in 2014. So if you plan or your premium has changed since 2014, it is no longer a grandfathered plan. (http://www.ciswv.com/CIS/media/CISMedia/Documents/Self-Insured-Plans-Under-Health-Care-Reform-070312_1.pdf)

Let me know how you make out with the insurance commission – great job continuing to fight them on this! We need more people to keep fighting until insurance companies finally get the message that they can’t walk all over us anymore!!

Thank you. Just found out at my second appt the front desk at OB told me I didnt have any coverage at all. I felt like bursting in tears. Come to find out calling the insurance my current OB bills global and the insurance says that is coded as a surgery and I don’t have surgery coverage at all. Insurance advise me to go on their website find all in network OB (which my DR is listed) but then I keed to call directly and ask if they are non global. Then I will be covered. I already feel defeated! So I buy insurance and think I’m covered but now I’m not because of medical billing codes??!!! Just insane!

Thank you so much for this article.

I’m so sorry this is happening to you. A couple pieces of advice… first, you should call your insurance and tell them that even if they aren’t covering the “surgical” or “diagnostic” portion of the global OB bill, they are required by the ACA to cover prenatal visits and other tests required during pregnancy as preventative care. If those are included in a global bill, they are required to pay a portion of the bill (usually around 40-50%). If they push back on this, file a complaint with your state insurance board immediately. This is federal law, so they WILL be forced to comply if you push hard enough. Unfortunately, you may still be stuck with the diagnostic portion of the bill (delivery) – however, check with your state insurance board, because I believe childbirth and prenatal care are considered essential health benefits and must be covered in some form (not necessarily 100% covered, but it should at least apply to your deductible). Good luck!

I absolutely have to jump in on this conversation. I have been the Billing Manager for an OB/Gyn for 13 years. Unfortunately, your information is not correct. The Global OB Code has been the standard for all commercial insurances for a very long time (sorry, I don’t know t the exact date it came in to effect). It is regulated by the American Medical Association. While I despise the “Affordable Healthcare Act”, it has nothing to do with this, and your physicians are NOT trying to rip you off. We would love to bill each visit and get paid for each one right away, but our hands are tied by the Global Fee. We see a patient for 9 months and cannot bill a dime until delivery, only to get paid a very small amount. So if you think this is something that was cooked up by doctors to scam patients, and you feel the need to put the information online, you need to do the proper research first.

Hi Chris, I appreciate you jumping in, and I agree with you the physicians are NOT the ones trying to pull one over on patients. Their hands are tied by the billing codes. I actually have a couple of screen shots in the post that show the insurance company fine print that requires doctors to bill using those codes. I can’t speak to when other insurance companies instituted global OB billing but my insurance company (Harvard Pilgrim) began the practice in 2012. My problem with global billing codes has nothing to do with doctors (I love my OB!), it is how insurance companies use them to lump both preventative and diagnostic prenatal appointments into the same claim so that they can file the claim as diagnostic and apply it to the member’s cost sharing/deductible rather than them having to pay the full amount (as required by the ACA for preventative care). Whether you believe the insurance companies did this on purpose in response to the ACA preventative care mandate, or perhaps it was an oversight, the outcome is illegal (on the part of the insurance companies, not the doctors). I have done extensive research on this issue and actually made a case against my insurance company in partnership with my state legislator, the result of which was them refunding all of their members that were overcharged in this way, as well as changing the way they file and pay Global OB claims. It’s great progress and I’m currently working to ensure other insurance companies do the same!

Thank you for writing this post…. you cleared up a lot of questions in my husband’s and my minds. We have been going back and forth between the insurance company and ob/gyn office trying to figure out what was going on. The ob/gyn set us up with a payment plan, so we would be paying during the pregnancy, instead of getting the bill at the end, but something didn’t seem kosher with what we thought our insurance should be covering. So after talking with the ob/gyn billing office again today, she basically revealed to us that a way around it would be if we switched practices then the new practice would have to bill each appointment individually instead of globally, since we had already begun the care at a different practice. So in this case our costs should be covered as stated in our policy. So I think this sounds like the easiest option to avoid having to fight the insurance company. Any insights on that?

I will definitely be sharing your article with everyone I know and encouraging people to research their bills and insurance., not just blindly pay them. Thank you so much for sharing your experience!

That does sound like a good option if you don’t want to have to fight your insurance company on it. If your policy states that prenatal visits are covered as preventative you should be able to get them to pay it either way but if your wife isn’t super attached to her OBGYN switching practices may be easier than battling the insurance company. Good luck!

As an aspiring out of hospital midwife, I’d like to know what can be done to help families? Should midwives and OBs start billing/coding each visit separately? Then charge a “delivery” fee? Would that make a difference? Would insuran e companies accept those claims and pay appropriately?

Hi Jessica, that’s a great question. Unfortunately most providers have their hands tied in this regard, because insurance companies typically require providers to bill using the global codes. I do think it would be helpful if providers kept a record of the individual appointments with notation about which are or would be coded as preventative and which are diagnostic/elective. That way when patients challenge their insurance companies and ask them to pay the preventative portion of the global bill, they have a written record they can provide proving the percentage of preventative appointments.

Hi, I have a question and would like your advice about the global on billing

Hi Heather, feel free to send me a direct message on Instagram (@ohbabyrichards) and I’ll help you out as best I can!

This is fantastic. Thank you for such an informative and helpful article! Delivering in around 3 weeks and feel so much more prepared.

Hi, I just recieved my hospital bill and my OBGYN’s bill. Something seems wrong. I’m being charged Obsterocal care fees by the Hospital ($4420.95) and by my OBGYN ($4455). My OBGYN didn’t deliver my baby, nor did anyone associated with her practice. When I was ready to deliver my doctor’s associates who had been on call were leaving for the night so instead of contacting my OB to come in (like they were supposed to) the nurses decided to have the Hospital’s resident OB deliver my baby. Once I had my baby, my doctor was called to come in to check in on me and to do my checkup the next day. It seems odd to me that I would have to pay two in patient obstetrical care fees. I attempted to contact my insurance company but they are giving me the run around. Based on my doctor’s bill it looks like they billed pre & postnatal care separately from my actual delivery date. I tried calling her office but they seem to feel that their charge is legit. What’s weird is that her office even charged for harvesting stem cells, which she wasn’t even there for. I was charged a lab fee by the hospital too so I’m wondering if that is also for stem cell harvesting. It feels like I’m being double charged but I have no clue what normal labor/delivery/hospital costs are and I stupidly didn’t check while I was pregnant. I’m kind of at a loss on how to handle this. I’ve had so many issues dealing with our insurance because of California’s insurance exchange I feel like I’m ready to lose it. Any suggestions on how I should proceed?

Hi Sara, insurance can be so confusing! I would start by calling the hospital and asking them to explain exactly what each of the charges are for. Then do the same with your doctor and compare. Make them be specific and don’t hang up until you fully understand each charge – that is your right! It is possible that the doctor is charging you for your pre and post-natal care (and not the delivery) or that they are charging you for the doctor’s visit after you delivered. If they are still charging you for the delivery – and the hospital is charging you for that as well I would absolutely fight it with your doctor’s office. Unfortunately if they refuse to rescind the charge you may need to get a lawyer, which considering the amount of the bill could be worth it. Also – make sure that you insurance company is covering the preventative portion of your pre- and post-natal care (as outlined in my post). When they lump it all together likes that the insurance company often passes the charge on to you, when they should be covering the preventative portion. Good luck!

Hi there,

How can I get in touch? I’ve been in tears all weekend and I’m 27 weeks pregnant with my first baby and I believe this is exactly what’s happening to me. I’m was with Aetna and switched to Kaiser January 1 during open enrollment and my Dr knew in my first visit that this was the case. I was told things were being approved and covered by my insurance and now we are in February and I’ve been individually billed for almost $9,000 in pre-natal care visits, lab work, ultrasounds, genetic testing that was highly recommended due to my high risk age of 38 (BS!). Aetna doesn’t want to pay, I’m no linger a customer, and they are blaming my deductible and the way my doctor coded the bills. I’ve talked to so many Aetna insurance staff and the doctors administrative staff which all just push me back and forth and give me the runaround. Meanwhile I have 800 #s hounding me for payment everyday. It’s causing me so much stress during my first pregnancy and worrying me that this could effect the health of our baby. This article was the first that came up when I typed in unfair medical billing for prenatal visits and has finally given me some hope. Thank you for posting this!

Hi Jenny, so sorry to hear you are going through this. Are all the bills you are receiving from prior to January when you were still covered by Aetna? If so it sounds like your doctor is billing the appointments individually and not with a global OB code, which is appropriate in your case since you switched insurance plans. It sounds like the issue you’re having is not so much a global OB code, but rather that the charges are being applied to your deductible and not covered as preventative. Unfortunately, when it comes to ultrasounds and genetic testing, your insurance is not required to pay those as preventative. They should cover them, but depending on your plan they would most likely be applied to your deductible and you would be responsible for the cost until you hit that deductible. What SHOULD be covered in full is your regular prenatal checkups and any routine tests like urine cultures, gestational diabetes testing, vaccinations, etc. If they aren’t paying those bills than you can absolutely fight them. Depending on the way your plan is worded you may be able to get them to reprocess the bill – OR – if the plan states that those things are subject to deductible you will likely need to involve your state insurance commission to help you fight them, since they should be paying those claims as preventative per the ACA BUT some insurance companies still aren’t doing that and you have to fight them on it. If you want to send me more specifics around your plan and what you are being billed for I’m happy to look it over and give you my thoughts on next steps – although I am by no means a lawyer or health insurance expert – just a mom who’s been there done that! You can email me at hannah.r.richards@gmail.com if you’d like. Good luck!

Hi! I wanted to first thank you for being here to help us understand what is going on with all of this billing stuff when it comes to pregnancy. I have a situation and after searching and searching, I came across your blog. I am really hoping in can borrow a few minutes of your time so you can help me fight my global fee. I am 20 weeks along. I came home last night to a bill from my OB office telling me that based on my current deductible ($5000) they were going to start charging me my global fee now and wanted me to start paying $400 a month from here on out. This is ridiculous to me. I did some research and apparently this is very common, what happens in my area (las Vegas) they charge global fees up front, then after the birth they charge the insurance, and then the reimburse you what is necessary. I refuse to do this. How can I get my OB to charge the global fee after my delivery ? I don’t want to pay for something up front that I haven’t even received yet and then wait around for a reimbursement. How do they know I won’t have to have my deductible met before then ? I don’t want to change OB since he delivers at the hospital I want to deliver at.

Hi Rocio, sorry you are dealing with this. Unfortunately it is quite common for OBs to pre-bill their global OB fee. They do this because insurers often don’t cover a large portion of it, and they don’t want to end up having to chase patients down for payment. Your doctor is within his or her rights to do this, so if you truly don’t want to pay up front you may have to find a new OB that doesn’t pre-bill. Once you give birth, however, you should make sure your insurer is paying their fair share of the bill – and your doctor will reimburse you. If you have for some other reason met your deductible by that point, the insurance payment to your doctor will reflect that, and your reimbursement from the doctor will be higher.

My advice would be to keep all receipts for payments made, and request an itemized statement of what is being billed and/or included in the global fee. When your insurance pays the doctor after delivery, request to see the EOB (explanation of benefits). If the insurance company isn’t paying at least 40% of the global OB fee (which is for preventative prenatal care) than you have a case against them. Unfortunately, your doctor is kind of trapped in the middle – he or she isn’t doing anything wrong by charging a global OB fee, and they are smart to try to collect it up front since insurance companies so often don’t pay it – even when they should be. So if you love this doctor I would pay the monthly fee and make sure to fight your insurance company afterward if they don’t reimburse you.

You could also attempt to talk it through with your insurance company up front and confirm with them that they are going to be paying at least 40% (the preventative prenatal care portion) of your global OB fee (if they say they aren’t paying the preventative portion I recommend reading through some of the responses I’ve made to other comments for advice on how to fight them). If you can get in writing from the insurance company what portion of the global OB fee they will cover, you can take that to your doctor and they may lower the amount you have to pay up front since they have confirmation from the insurance company that the remainder will be reimbursed.

Good luck, and let me know how you make out!

Hi Hannah,

I just wanted to say thank you for writing this article. Global OB billing & coding is confusing and I think you did a great job explaining it. I work for an OB/GYN clinic and, as you have mentioned, we really do have our hands tied when it comes to billing. Most plans require us to bill a global OB charge and will deny our claims if we separate them. I do everything I can as the billing manager to advocate for our patients so that they’re getting the most out of their insurance company. Anyway – just wanted to write a quick thank you for the thorough explanation.

Hi Taylor – thanks for your message. I definitely understand how doctors have their hands tied, and I know the billing you have to do is crazy complicated. Thanks for trying to advocate for the patients at the practice where you work!

I am in the thick of this right now. Beautiful bill for $2,800 dollars that has a global code and the cherry on top is that it’s dated last year so that I didn’t meet my deductible so I have to pay it out of pocket. I found out that it was all applied to cost sharing. Multiple insurance reps practically yelled at me that the bill did not have any prenatal visits included, but then why was it dates back to the date of my first prenatal? After two or three supervisors, it was confirmed that it includes 7 prenatal visits. So why do I have to pay for it? They are making me file a dispute. Any tips for information I can include in the dispute?

Thank you so much!!

Ugh, so sorry to hear that Amanda! That is exactly what happened to me. In the end, though, they did pay my bill! I would start by reading through all the comments here (I link a lot of different resources) – and then check out this update post, if you haven’t already: https://ohbabyrichards.com/2018/12/28/victory/. You may be able to use some of the documents I used with Harvard Pilgrim as examples, or at least help you frame what you’re asking them to do. I also strongly encourage you to get your state insurance commission involved – filing a claim with them can really help move things along. The first thing I would do is confirm that prenatal visits are covered as preventative under your particular plan – if you can find that in writing somewhere, you will have a very strong case for forcing them to cover at least a percentage of your global bill. Feel free to DM me on Instagram if you have specific questions that I might be able to help you with!

Hi Amanda,

I work in an OB/GYN office in the billing department. Ask your insurance company which CPT codes were billed for each claim that is causing you problems. CPT 59426 is for 7+ prenatal visits only. 59400 is the global vaginal delivery code. Per coding guidelines, the global delivery codes should be billed on the day of delivery, they shouldn’t back date to your prenatal visits. I’d be happy to help. I love writing insurance appeals 🙂

Thank you Taylor – that’s great info!

How do I get in contact with you about this issue for i have done a little battling myself, and you have woke the fight in me once again. you have provided me with more ammo for the fight.

Hi Nicci, I just sent you an email at your gmail address, let me know if you didn’t receive it 🙂

I just tried to contact my insurance (BCBS) and see what their system was for global billing, just to see so I could be prepared (due in November) and the lady I spoke with was trying to tell me that prenatal visits aren’t covered under the Affordable Care Act, because it’s considered “medical” and not “preventive” -_-