This blog post is about 2 years overdue, but, just like I say about remembering to bathe my kids, better late than never.

Back in 2016, a few months after Lucy was born I wrote a blog post. It was called The Global OB Fee Trap: How to Find and Fight It. It was a very long-winded rant about how my insurance company at the time incorrectly (err, illegally) processed my prenatal care claims and how I bitched at them for long enough that they eventually paid them.

I wrote the post because I was broke and angry and on maternity leave, which is when I typically sleep little enough that I have time to do things like write blog posts. I assumed nobody would read it because everyone knows our healthcare system is fucked and nobody wants to listen to one more hormonal mother rant about it.

Wrong.

Apparently I am not the only broke and angry mama bear out there. Within a few months the post started ranking in Google search for any and all terms related to Global OB or maternity billing. And apparently people search for those terms kind of a lot.

The comments and messages started pouring in from moms, dads and parents to be – telling me they were facing the same issues and asking for advice on how to fight their insurance companies. I was overwhelmed and out of my league because I am not a lawyer, I am not a doctor, and I don’t play either of those things on TV (but hey – hire me!).

Add to that the incredible complexity of each individual insurance plan and company, each state, and each state agency’s differing interpretation of the absurdly vague and constantly changing Affordable Care Act requirements. I felt helpless.

So I did what I always do when I feel lost and confused. I Googled it.

Seriously I Googled the shit out of the ACA, Harvard Pilgrim, benefits administration, healthcare laws, preventative care guidelines. Pretty sure I now know more about the ACA and healthcare administration than any of our elected officials and DEFINITELY more than the leader of the free world. *Facepalm*

And you know what happened? I got fucking pissed. Because I realized how many woman were getting blatantly screwed by their insurance companies during a time in their lives (postpartum) when they especially don’t want to be screwed by ANYONE – including their significant other. Take the hint, guys.

So I did what any over-parented only child would do and I called my dad. I raged for like 20 minutes until he was like, WTF are you calling me for – call someone that makes the rules. Which is when I got that really sad feeling that you get every time you’re like “Moooooooom what’s for dinner?” And then you realize you are the mom. Adulting really is the worst.

But eventually I got over my sad, entitled and pathetic Millennial self and called my State Senator, Cathy Breen. She ignored me, but I don’t blame her because she probably gets like 100 emails a day from people whining about how much their insurance costs.

So I emailed her like 450 more times until one of her staffers was finally like, please Cathy, go meet with this girl so she will stop harassing us. This is how I have achieved most things in life, so, sorry to every customer service or support person I have ever interacted with!

I met with Cathy at a local cafe for coffee, and she was very nice and I think a little surprised at the depth of research that I presented to her regarding the Global OB billing scam that insurance companies are pulling on postpartum moms. Similar to me, her first reaction was “we can’t be the first people to discover this – there must already be some kind of legislation in progress.” I assured her that if there was, it was not on Google, and accepted her offer to “look into it” and “get back to me.”

Now, I speak public servant pretty fluently and I know that that is code for, please forget about it. But to Cathy’s credit (who was just recently re-elected – yay!) she DID look into it and she DID get back to me. In fact, she contacted the state Attorney General and basically wrote a letter to Harvard Pilgrim asking if they were aware of the issue and pressuring them to cut that shit out.

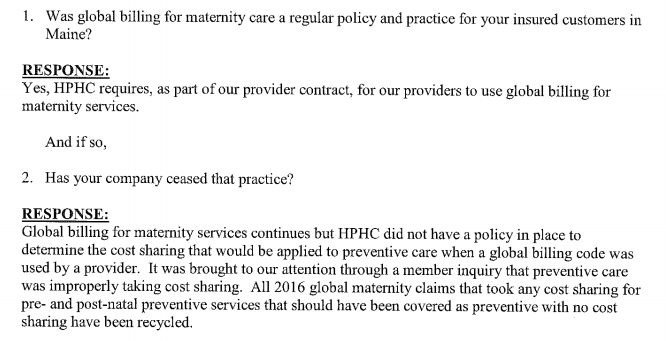

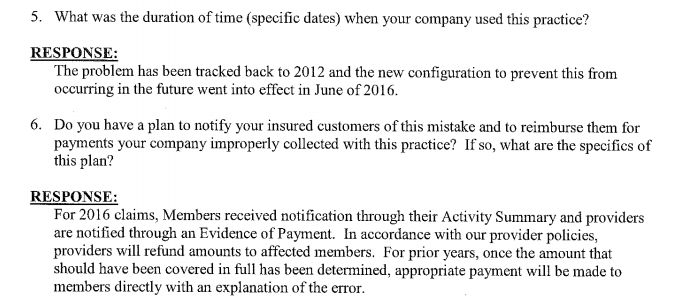

All this took place over the course of like 5000 years (ok fine, like 6 months) but eventually Cathy and I received a letter from the Associate General Counsel of Harvard Pilgrim acknowledging their error, and informing us that it had been corrected. Here are a few of the more exciting excerpts from the letter:

When I received that letter I felt more victorious than when I originally convinced them to pay my Global OB bill. I did a little dance and of course called my dad who assured me that I was in fact, the greatest.

But despite my little victory dance I continued to receive emails every week from other parents in other states (and with other insurance companies) who were up against the same issues and feeling helpless. I have come to terms with the fact that I probably won’t be able to fight this on a national scale right now (although there are days where I get really fired up) but I do try to respond to each and every email, offering support, resources, whatever knowledge or advice I feel is relevant – and encouragement to fight the good fight, even if it feels unlikely to result in a win. Because it is going to take a village to fight this battle. A whole tribe of angry mamas (and dads!) putting the pressure on HARD.

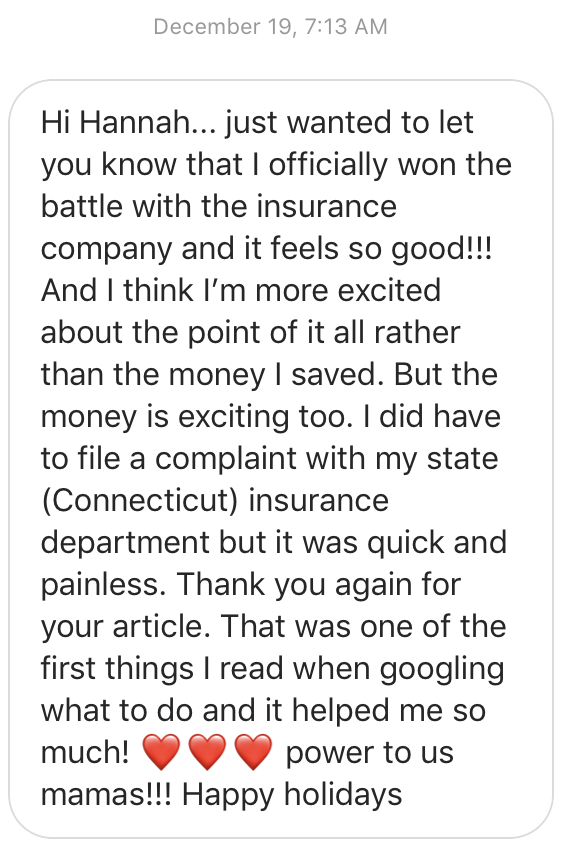

And then last week I got this message from a new mom I had been chatting with months earlier on Instagram – and it felt like the biggest victory of all.

I literally did a happy dance right there at my bathroom sink. You guys – WE. CAN. DO THIS. We are doing this.

You know Millennials get blamed for basically everything that goes south these days – from napkins to fast food – even marriage. But here’s something else you can happily add to our hit list: bullshit insurance policies.

We are “just a bunch of Millennial moms” who are slowly, collaboratively and skillfully changing the healthcare landscape and beyond.

Watch. Out. Patriarchy.

These mamas are coming for you.

I want to fight my OB office. I was just told after 3 visits they want to put me on a payment plan that I can’t afford. I informed them I have other bills going toward my deductible each month and my deductible will be met soon. This is only for office visits, but I will confirm. Office visits are not expensive and are paid 100% after deductible is met. This is really stressing me out and I’m sure it stresses out a lot of pregnant moms. I didn’t have to do this with my first one.

Hi Rachel, sorry to hear about your situation. Unfortunately there’s not much you can do if your OB is operating outside of a public hospital (in which case you would likely be able to work out a plan with the billing department based on your income). Even though I know it’s frustrating, your OB isn’t really the one to blame here – most have taken to billing patients ahead of time for prenatal care since it gets billed to insurance in a lump sum at the end (global OB billing), and insurance companies are so adept at getting out of paying it that OBs are trying to protect themselves (and their patients) from getting a large lump sum bill after the baby is born. Legally they can bill you however you want and the only way around it is either working with them on a payment plan that works for you – or finding a new doctor. It sucks, I know! That said – your insurance SHOULD cover the cost of all those prenatal visits in the end once the global OB fee is billed (you will be responsible for the diagnostic portion of the care – i.e. delivery, hospital charges, ultrasounds and any other diagnostic tests). If you don’t see your insurance company covering at least 40% of the global OB bill (the preventative care portion) definitely fight them on that!

Hannah,

My State Representative here in Florida is willing to take on Cigna, one of the largest insurance companies, but the thing they said would be the most helpful for them to see is the entire letter and the responses you received to your State Representative’s letter. Do you have a copy of it you could upload somewhere or could email me directly? My wife and I are suffering through this “Global Fee” scam right now and the insurance company refuses to budge; instead we are supposed to pay a $1700 bill while both of us are unpaid for the next 3 months.

Hi Stuart, so sorry to hear you are going through the same thing -it’s the last thing you want to have to focus on with a new baby in the house! If you can send me your email I would be happy to send you the documentation that I have from Harvard Pilgrim. Thanks for taking on the fight!

Hi Hannah,

Dealing with the same issues that you mentioned with the Global Fee with my insurance company plan and OB/midwife office here in Georgia.

Trying to understand the exact steps I should take to at least fight that the insurance company should pay for at least the preventative portion of the Global Fee, but I’m unsure what to do and how to determine that. Any advice here?

Would love to reach out to you if you’ve provided the same information to other readers. Is there a way to contact you privately? Thanks so much for speaking out and helping other parents!

Hi Amy, sorry you’re going through a similar fight with your insurance company It’s so stressful. Have you read through the other two posts (https://ohbabyrichards.com/2016/07/19/the-global-ob-fee-trap-how-to-find-and-fight-it/ and https://ohbabyrichards.com/2016/07/19/how-to-fight-your-global-ob-fee-bill/)I have on the subject? There are some good tips in there for fighting your insurance company, as well as some additional documents, etc. in the comments on those posts as well. If you have contacted your insurance company already and they are refusing to pay, filing a claim with your state insurance commission is probably the best next step. Take a look through those posts and the comments and let me know if you have additional questions, I’m happy to help. The best way to reach me is direct message on Instagram (@ohbabyrichards) 🙂

It’s so stressful. Have you read through the other two posts (https://ohbabyrichards.com/2016/07/19/the-global-ob-fee-trap-how-to-find-and-fight-it/ and https://ohbabyrichards.com/2016/07/19/how-to-fight-your-global-ob-fee-bill/)I have on the subject? There are some good tips in there for fighting your insurance company, as well as some additional documents, etc. in the comments on those posts as well. If you have contacted your insurance company already and they are refusing to pay, filing a claim with your state insurance commission is probably the best next step. Take a look through those posts and the comments and let me know if you have additional questions, I’m happy to help. The best way to reach me is direct message on Instagram (@ohbabyrichards) 🙂

I am currently pregnant, living in Ohio, but high risk due to age and other medical issues. I have 100% maternity coverage, no copay, no deductible (through a plan through the post office). My high risk provider doesn’t do global maternity billing. My insurance company said I can send all the claims back after the baby is born to be reprocess as global maternity. However, every claim that was processed shows a copay of $20 and they are piling up quickly due to my frequent visits. Any suggestions on how to fight this? Right now I am collecting all of my eobs in a folder.

Hi Jennifer, if you have 100% maternity coverage with no copay or deductible, you should not be charged a copay for your office visits. I would verify with your insurance company that you do not in fact have any copay, and then relay that information to your doctor and refuse to continue paying the copay. If they argue, arrange to have a 3-way call with your insurance company and your doctor’s billing office so that they can communicate directly with you on the phone. Ask for everything in writing. This sounds like a misunderstanding of your benefits/coverage more than a global billing issue so hopefully you can get it worked out quickly!

Hello! I read your blog posts before my first OB appt and even brought this up to my insurance (bcbsil ppo) and they were adamant that pregnancy is a “diagnosis” and nothing would be considered preventive care/covered 100%. The only thing they said that would be considered preventive are annual physicals and well-woman exams (outside of pregnancy).

I also looked at the ACA language and now im confused all over again. Please help, thanks!

So sorry you are up against this. I have heard this from a few other people as well with BCBS. I have a few tips below on how you can fight them – but I also recommend contacting your state insurance commission to report them in violation of the ACA. I had a lot of success working with my state senator to help get these types of policies changed. In terms of convincing your insurance company that prenatal checks up must be covered without cost sharing (you should NOT be charged any copay whatsoever for the prenatal visits unless the copay is for diagnostic testing that was administered during the visit) you can use these links. The first link (https://www.hrsa.gov/womensguidelines/) outlines what services MUST be covered as preventative care. You will see that many of the tests you receive during pregnancy such as immunizations and prenatal diabetes screenings should all be covered in full without cost sharing. That list also includes well-women visits. You can see that there is an asterisk in that column that says that the frequency of well woman visits is dependent on a women’s health status. A healthy (non-pregnant woman) only gets one visit per year, but pregnant women are entitled to additional covered well-women visits (i.e. prenatal checkups). If you look at this second link (http://www.healthlaw.org/about/staff/susan-berke-fogel/all-publications/well-women-visits-prenatal-care-under-the-acas-womens-health-amendment#.WZ2k2XeGMmI) it breaks down the subtext of the ACA bill which specifically states that women require multiple well-women visits during pregnancy, and that even more well-women visits are warranted for high risk pregnancies. Take a look at the text in here and present it to your insurance company as evidence of their responsibility to cover the prenatal visits (and other covered services during those visits) in full. Let me know if you have further questions – but definitely fight them on this one, the law is on your side!

Hi Hannah – you rock.

I’m 25+ hours into researching what to expect with global billing. I’m due in February 2020. The hospital and doctor do global billing so I have not yet received a bill outside of labs and ultrasounds.

I’ve talked to the insurance company 5x (every time I get a different answer and they say “talk to your doctor”). My doctor says the insurance company has the answers. I’ve talked to 3 insurance experts and the hospital where I will deliver 4 times. I’ve never gotten a straight answer “because the bill hasn’t been submitted yet.” My dad used to oversee billing for a hospital and I talked to him too, plus a friend who’s currently in the industry in IL but I live in WI and apparently this differentiates by state…

What I’m trying to find out is if I switch insurance companies in 2020, to a better plan with copays and $0 deductible, from the HSA/HDHP plan that I am on in 2019, how/will the bill be split. Will the hospital bill both insurance companies? Will the bill be split up by the dates of service from prenatal in 2019 and delivery/postnatal in 2020? Or will the 2020 insurance company just be responsible for all of the “global bill?”

If the bill will hit 2 insurance companies with 2 different out of pocket maximums, I could be paying double if I change insurance. And if I stay with the same crappy insurance, it might not even matter, because they might charge me against the service dates in each calendar year, going to 2 different deductibles anyway. Efff!!!

I have to make a decision by 12/13/19 if I want to enroll in a different, “more affordable,” marketplace-offered HDHP plan. Or I can move to my employer’s copay insurance as of 1/1/20.

Did you run into split year global billing at all in your research?

Any idea who I could call who I haven’t called already?

Help!

Hi Sarah, I haven’t been in this situation and I think it is probably a little bit different with each insurance company so unfortunately I don’t have a good answer for you. I would call the new insurance company and push them for more answers. Their first line of customer service won’t know but if you stay firm they should escalate your call to someone with more information. If your insurance is through your work, your work likely also has an advocate that can help you (ask HR) they would be able to put you in touch with your company’s insurance broker.

It might also be helpful to organize a 3-way call with your insurance company and your doctor to force them to talk to each other. Basically, everyone wants to send you to someone else to deal with it in these situations and so you have to be firm and force people to listen to you and provide solutions. It’s not easy, I’m sorry you’re having to deal with it. My guess is that your doctor will have to bill the prenatal claims to your current insurance, and then bill the delivery/postnatal to the new insurance, but you’ll need to make sure they do that correctly in order to get the claims paid by insurance (that is why a 3-way call might be useful). Here is some info I found online stating how multiple insurance carrier pregnancies should be coded: “Billing for the antepartum (prenatal) visits must be divided between 2 different insurers. Use the code 59425 (4 to 6 antepartum visits) or code 59427 (7+ antepartum visits) to bill each carrier separately and then bill the current payer for the delivery and post-partum care using the code 59410, if it is an uncomplicated vaginal delivery.”

This might also be a useful resource: https://www.supercoder.com/coding-newsletters/my-ob-gyn-coding-alert/reader-questions-coding-a-pregnancy-when-a-change-of-insurance-carriers-has-occurred-article

In terms of the deductible, since it is a new plan year you will have to pay separate deductibles, but it sounds like the new plan doesn’t have a deductible so it shouldn’t be too much of an issue. Also your prenatal visits that will be billed to the old insurance SHOULD be covered in full as preventative well-woman care, so it shouldn’t impact your deductible there. As far as the hospital – they only become involved for the delivery so as long as you change insurance before you deliver the hospital bill will just go straight to your new insurance. The bill from the hospital is separate from the global OB bill submitted by your doctor. Sorry I can’t be more helpful!

This is the most helpful response I’ve received to date. Thank you. My current insurance charges 20% coinsurance for prenatal office visits 😦

Just sharing a follow-up comment to my post from yesterday. I found this on the Humana website:

https://www.humana.com/provider/medical-resources/claims-payments/claims-payment-policies

A Humana plan does not provide benefits for expenses incurred while the patient is not enrolled in the plan. Therefore, Humana will not reimburse a charge for a CPT code that represents a set of services unless all the services were provided while the patient was enrolled in the plan. All statements below are limited by that reimbursement limitation.

Seems that if I moved to their plan, I’d be required to pay out of pocket for the 2019 expenses under my current HSA plan.

Hi Hannah! Pregnant with baby#5 and this is the first time I’ve ever had to deal with this global fee stuff and it’s so confusing! I was literally just given a paper at my OB saying this will be an estimate of your global fees, have a nice day.

I know with my ins that I have a $25 copay for each visit and $500 per day hospital. I’m estimating healthy pregnancy should be around $18-1900. Their paper said $2500-3k. 😮 I have a feeling I’ll be in for a fight, but until I get that bill I won’t know for sure. So I should at least start saving what I know my deductibles are, because I’ll be paying those towards my ins no matter what, right? I haven’t gotten a statement yet, so every time I go in I’m switching money over to savings like I paid something so it’s there for later. Thanks!

Hi Sarah, it definitely is confusing. Since you are trying to prepare I would definitely save the amount of your deductible so that you have the money saved when you need it. The reason the global OB fee they are quoting is more than you expect is because it includes the doctor’s fee for delivering the baby, as well as all of your pre and post-natal appointments. The hospital fee will be a separate bill. Your insurance will pay a percentage of the global OB bill once it is submitted, based on your cost sharing setup. The thing you want to watch out for is that the insurance pays the correct portion. They should cover your prenatal care as preventative (i.e. you pay nothing) and you should only be responsible for the delivery charges. Most insurance companies that pay these claims correctly split the OB bill on a percentage basis – somewhere around 40% preventative (they pay that) and 60% delivery charges (you pay that). It’s really hard to give you a specific answer without knowing the specifics of your insurance but I highly recommend setting up a conference call with you, your doctor’s billing department and the insurance company so that you can understand exactly how much you are going to be responsible for and make sure they are paying the correct amount. Good luck!

Hi Hannah!

For.it is somehow the other way around: My insurance (United Healthcare) is conforming full coverage with no patient responsibility for prenatal prebentative care as described under the ACA but the provider is billing at first visit a global maternity package requesting me to pay about $1600 for all my upcoming routine prenatal care visits until 6 weeks postpartum. And they say that this does not include ultrasounds imaging…

But again, my carrier confirmed that all this should be with no patient out of pocket.

Hi Marta, your doctor’s office probably charges that fee upfront to cover any portion of the actual delivery fee that your insurance doesn’t cover. It sounds like your insurance covers prenatal care in full which is great, but you likely do have some form of cost sharing for the actual delivery (diagnostic care) – typically between 20-40% depending on your plan. I’ve actually worked a little bit with United Healthcare and last time I checked they are one of the companies that DOES split up the global OB fee so that you are only charged cost sharing on the diagnostic portion (delivery)s. on the entire fee which includes prenatal care. Your doctor’s office is billing for this upfront to cover themselves in case you don’t pay up, but if your insurance company ends up paying a larger portion your doctor’s office will refund you the difference. Best wishes for your pregnancy and let me know if any questions come up when you get the final bill 🙂

Hi Hannah,

Firstly, thanks for sharing your experiences! It is encouraging to know that we have some power to make change in this crazy system. I am late to the party (first time dad-to-be), and stumbled upon your posts while trying to navigate our own prenatal insurance dilemma. My wife has been billed nearly 100% of the costs for pretty much all of her ‘routine prenatal’ visits, and we were under the impression that these should be fully covered by the Affordable Care Act. [We are in California.] After several months of exchanges with the benefits specialist from USI insurance, we finally received a partial answer today, indicating that “… Her pregnancy is considered high risk, so the standard prev maternity benefits are not provided due to her high risk DX…” For added context, my wife is only considered high risk because she is 35, and for no other reason. She is extremely health conscious and has no prior medical issues. If this is the actual reason they are using to deny coverage, we will definitely fight them on this. English is my wife’s second language, and all of the jargon in these ‘explanations of benefits’ also has me confused as a native speaker. I have no idea how anyone navigates this system, and miss living abroad lol.

Anyway, that’s my rant. With that said, glad your case (and your war) was won! Wishing you and yours all the best.

-Dave

Hi Dave,

That’s really messed up what is happening to your wife – I’m so sorry! I would definitely push them on paying for those routine visits, and if they don’t resolve it, I would file a claim with the CA insurance board. Congratulations on becoming a dad – hope you’re able to get this resolved soon!!

Hannah

Thank you for both the tip and the congrats 🙂

We will keep the CA insurance board in mind if we can’t resolve this directly with our insurance. Just wish we didn’t have to navigate this while prepping for a baby, but such is life in this “great” nation….. -_-

All the best!

Dave